7 Smart Things to Do If You Want to Avoid Lifestyle Inflation

Lifestyle inflation looks harmless at first. You earn more, so you spend more, and everything feels fine. I learned over time that without intention, higher income can quietly delay freedom instead of improving it.

What Is Lifestyle Inflation in Real Life

Lifestyle inflation happens when spending rises automatically as income increases. It rarely feels like a mistake because upgrades often seem logical, earned, and justified at the moment.

In real life, it shows up in small decisions. A better phone plan, more food deliveries, frequent upgrades, and higher monthly commitments slowly become normal.

The danger is not one big purchase. It is the collection of habits that lock you into a higher cost of living without improving long-term security.

I noticed lifestyle inflation when my income grew but my savings barely moved. More money came in, yet financial pressure stayed the same.

Understanding this pattern is the first step. Once you see it clearly, you can make smarter choices without feeling deprived.

1. Pay Yourself First Before Upgrading Anything

One of the smartest things I ever did was changing the order of my money decisions. Instead of upgrading my lifestyle first, I prioritized saving and investing.

When income increases, it feels natural to reward yourself. The problem is that rewards quickly turn into expectations and fixed habits.

Paying yourself first means setting aside savings immediately. What remains becomes your spending limit, which naturally controls lifestyle expansion.

Automation helps remove emotion. When money moves out before you touch it, temptation loses power.

Ways to pay yourself first include:

- Automatically increasing savings after raises

- Sending money to separate accounts immediately

- Treating savings like a non-negotiable bill

- Adjusting spending to what remains

2. Set Lifestyle Rules That Guide Spending Decisions

Lifestyle rules changed how I spend without constant budgeting stress. Rules reduce decision fatigue and protect you during emotional moments.

Instead of asking if you can afford something, rules help you ask if it fits your long-term plan. That small shift changes everything.

For example, I stopped upgrading recurring expenses easily. One-time purchases feel different from monthly commitments that follow you for years.

Rules also help handle social pressure. When expectations are clear, saying no feels less personal.

Examples of helpful lifestyle rules:

- No upgrades to fixed expenses after raises

- Waiting periods before large purchases

- One lifestyle upgrade per income increase

- Avoiding spending to impress others

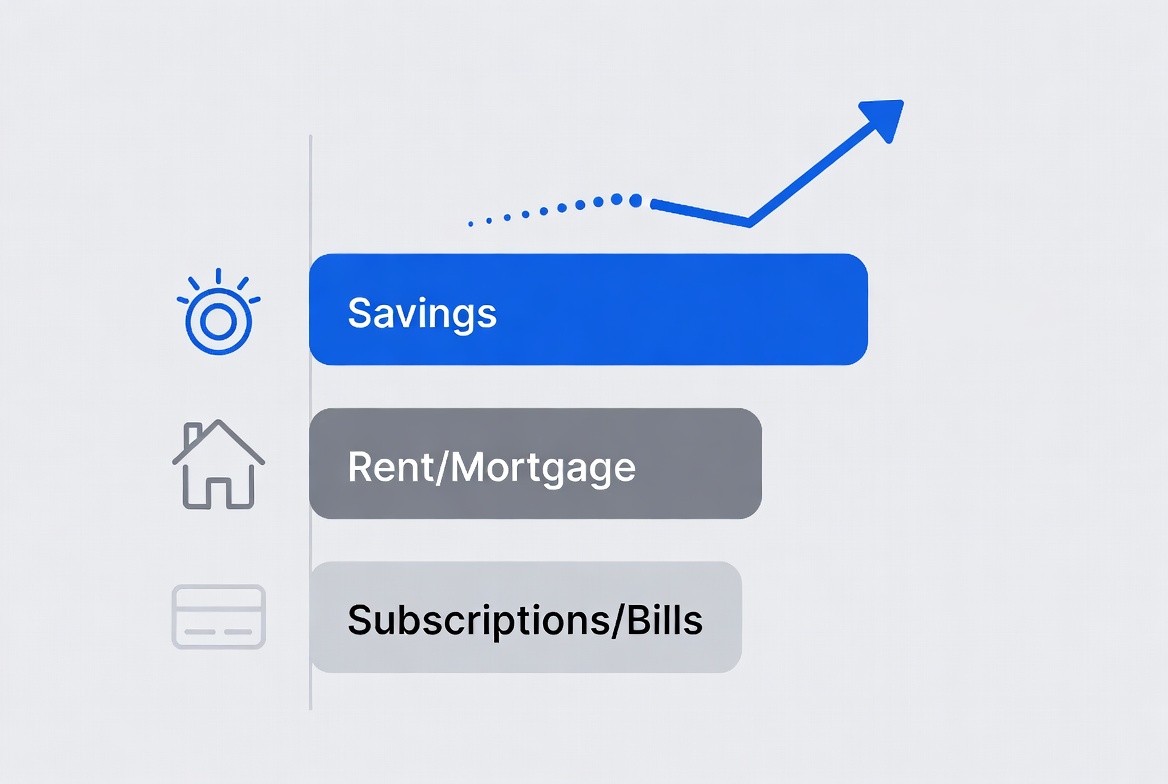

3. Increase Your Savings Rate, Not Your Fixed Expenses

Fixed expenses are the biggest drivers of lifestyle inflation. Rent, car payments, subscriptions, and insurance are hard to reverse once increased.

When income rises, increasing savings instead of fixed costs builds flexibility. You gain options instead of obligations.

I learned that flexible spending is easier to adjust during tough times. Fixed expenses lock you into stress when income fluctuates.

Raising your savings rate creates momentum. Progress becomes visible, which feels more rewarding than short-term upgrades.

Focusing on savings first does not mean never enjoying money. It means enjoying it without creating future pressure.

4. Separate Comfort Spending From Status Spending

Not all spending is bad. Comfort spending improves daily life, while status spending often serves external validation.

I had to learn the difference. Comfort spending supports rest, health, and peace. Status spending tries to signal success to others.

Status purchases often lose value emotionally quickly. The excitement fades, but the cost remains.

Comfort spending, when intentional, can increase quality of life without fueling comparison or competition.

Ways to tell the difference include:

- Comfort spending reduces stress

- Status spending seeks approval

- Comfort feels sustainable

- Status often creates pressure

5. Upgrade Your Skills Faster Than Your Lifestyle

Skills compound faster than material upgrades. When I focused on learning, my income became more flexible and resilient.

Lifestyle upgrades feel permanent. Skill upgrades increase earning potential without locking you into higher costs.

Learning new skills also builds confidence. You rely less on external validation and more on your ability to adapt.

Over time, skills give you leverage. You can earn more without immediately spending more.

Choosing learning over lifestyle upgrades delays gratification, but it creates options that last far longer.

6. Track Lifestyle Creep Without Obsessing Over Numbers

Tracking spending does not require extreme budgeting. Awareness matters more than precision.

I started by reviewing expenses monthly. Patterns became clear without tracking every transaction obsessively.

Lifestyle creep often shows up quietly. Subscriptions, convenience spending, and upgrades slowly add weight.

Catching these early prevents painful adjustments later.

Simple ways to track lifestyle creep include:

- Monthly expense reviews

- Watching fixed costs closely

- Noting new recurring payments

- Comparing savings growth over time

7. Practice Intentional Delays Before Major Purchases

Delaying purchases changed my relationship with money. Waiting removes emotional urgency and reveals true desire.

Most things feel less necessary after time passes. That pause often saves money without feeling restrictive.

I use waiting periods for large purchases. If I still want it later, the decision feels intentional.

Delays also prevent stacking commitments that raise monthly expenses unnecessarily.

This habit builds discipline quietly, without feeling like sacrifice.

Common Traps That Make Lifestyle Inflation Worse

Lifestyle inflation is fueled by subtle traps. Social comparison makes spending feel required rather than optional.

Subscription overload is another issue. Small monthly charges feel harmless but add up quickly.

Treating raises as spending permission is a dangerous habit. Income growth should create freedom, not dependency.

Ignoring these traps allows lifestyle inflation to grow unnoticed.

Common traps to watch out for:

- Comparing lifestyles with others

- Adding subscriptions without review

- Rewarding every raise with spending

- Normalizing constant upgrades

How Avoiding Lifestyle Inflation Improves Your Life

Avoiding lifestyle inflation creates breathing room. Money becomes a tool instead of a source of stress.

Savings grow faster, and emergencies feel manageable. You gain flexibility during unexpected changes.

Progress toward long-term goals accelerates. Financial independence feels closer and more realistic.

Emotionally, reduced pressure improves peace of mind. Less obligation means more freedom to choose.

Living below your means is not about deprivation. It is about control.

Final Thoughts

Avoiding lifestyle inflation does not mean avoiding enjoyment. It means choosing upgrades that serve your future, not trap it.

From personal experience, financial peace feels better than constant upgrades. Freedom grows quietly when spending stays intentional.

If you earn more but spend the same, your future thanks you. Small decisions today shape long-term comfort and confidence tomorrow.