7 Ways Inflation Affects Your Money and Investments

Inflation is one of those money topics people talk about like it is distant or technical, until it starts showing up in grocery bills, rent increases, and shrinking savings. I learned quickly that inflation affects daily choices more than big financial theories.

Why Inflation Feels Personal, Not Theoretical

Inflation becomes real when familiar prices change without warning. You notice it when your regular shopping list costs more, even though you bought the same items. That personal impact makes inflation emotional.

Inflation touches routines, habits, and comfort. It affects how secure you feel about money, even if your income stays the same. That emotional pressure often drives decisions before logic gets involved.

1. Your Cash Loses Buying Power Over Time

Cash feels safe because the number does not change. What changes is what that number can actually buy. Inflation slowly reduces the value of money sitting still.

Holding cash for too long means accepting less future value. Even modest inflation can erode purchasing power faster than most people expect.

Why the Same Money Buys Less Each Year

Inflation raises prices while cash remains flat. That gap grows quietly. A dollar today often buys less next year, even if inflation seems mild.

This loss is gradual, not dramatic. That makes it dangerous, because it does not trigger urgency until noticeable damage is already done.

The Hidden Cost of Holding Too Much Cash

Cash is useful for emergencies and short term needs. Beyond that, excess cash becomes a liability during inflationary periods.

- Savings lose real value over time

- Opportunities for growth are missed

- Confidence in stability can be misleading

2. Everyday Expenses Rise Faster Than Expected

Inflation rarely hits everything equally. Essentials like food, transportation, and utilities often rise faster than overall averages suggest.

This uneven increase makes inflation feel heavier than reported numbers. Daily necessities leave less room to adjust spending.

Groceries, Fuel, and Utilities as Inflation Signals

These expenses act as early warning signs. When basics rise, it affects everyone quickly, regardless of income or lifestyle.

People notice grocery inflation immediately. Fuel and electricity costs ripple into transportation, delivery, and service prices.

Why Budgets Break Even When Income Stays the Same

A stable income can still feel insufficient during inflation. Rising essentials quietly consume money once allocated elsewhere.

- Discretionary spending shrinks

- Savings contributions slow down

- Financial stress increases without clear cause

3. Savings Accounts Struggle to Keep Up

![]()

Savings accounts provide safety, but inflation challenges their effectiveness. Interest rates often lag behind rising prices.

This gap creates a false sense of security. The balance grows slowly while purchasing power declines faster.

The Gap Between Interest and Real Inflation

If inflation exceeds savings interest, money loses real value. Even positive returns can result in negative outcomes after inflation.

This reality surprises many savers. Seeing numbers increase hides the fact that buying power is shrinking.

When “Safe” Money Slowly Shrinks

Safety is about access, not growth. During inflation, safety comes at a cost.

- Reduced real value

- Lower future flexibility

- Opportunity cost over time

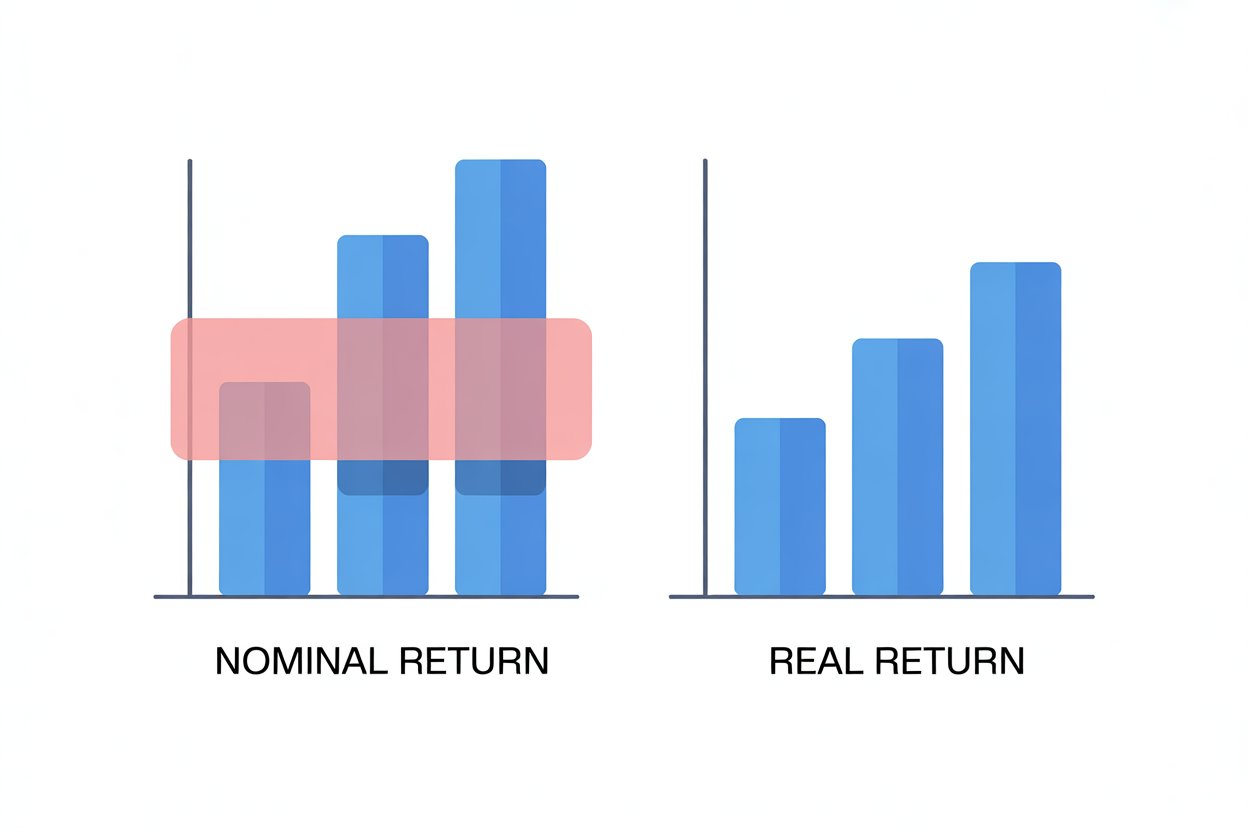

4. Investment Returns Look Different After Inflation

Investments are meant to grow money, but inflation changes how gains should be viewed. Nominal returns can be misleading without context.

What matters is real return, the amount left after inflation reduces value.

Nominal Gains Versus Real Gains

A ten percent return sounds impressive until inflation takes a large portion of it. Real growth may be much smaller.

Understanding this difference changes expectations. It also helps explain why some investments feel disappointing despite positive returns.

Why Some Profits Are Smaller Than They Appear

Inflation quietly eats into gains. Taxes and fees can compound the effect.

- Headlines highlight nominal growth

- Real value tells the full story

- Long term planning depends on real returns

5. Debt Can Become Easier or Harder to Manage

Inflation affects debt differently depending on structure. Fixed and variable interest behave in opposite ways during inflationary periods.

Understanding this difference can reshape how debt feels emotionally and financially.

Fixed Versus Variable Interest Rates

Fixed debt becomes easier over time if income rises with inflation. The payment stays the same while money loses value.

Variable debt often becomes harder. Interest rates may increase, raising monthly obligations unexpectedly.

How Inflation Changes the Weight of Debt

Debt does not exist in isolation. Inflation changes its real burden.

- Fixed payments lose real weight

- Variable payments can escalate quickly

- Planning becomes essential

6. Spending and Investing Behavior Shifts

Inflation does not just change numbers. It changes behavior. People react emotionally before adjusting logically.

Fear, urgency, and uncertainty often shape spending and investing patterns.

Why People Take More Risks or Freeze

Some chase higher returns to outrun inflation. Others stop investing altogether, waiting for stability.

Both reactions carry risk. Emotional decisions often ignore long term consequences.

Emotional Responses to Rising Prices

Inflation triggers stress responses. These responses influence habits and priorities.

- Increased price sensitivity

- Reduced patience

- Heightened financial anxiety

7. Long Term Planning Requires More Flexibility

Inflation challenges static plans. What worked five years ago may no longer fit current realities.

Flexibility becomes a survival skill rather than a luxury.

Retirement Goals in an Inflationary World

Retirement projections must account for rising costs. Ignoring inflation leads to underestimating future needs.

Long timelines magnify inflation’s impact. Even small miscalculations grow significantly over decades.

Why Static Plans Stop Working

Fixed assumptions break under changing conditions. Inflation exposes weaknesses in rigid strategies.

- Spending estimates become outdated

- Savings targets lose accuracy

- Investment strategies need adjustment

How to Adjust Your Money Strategy During Inflation

Adjusting does not mean overhauling everything. Small, thoughtful changes build resilience over time.

The goal is protection without panic, and growth without recklessness.

Protecting Purchasing Power Without Panic

Staying calm allows better decisions. Inflation rewards patience paired with awareness.

Diversification, consistency, and realistic expectations matter more than dramatic moves.

Small Tweaks That Add Long Term Resilience

Minor adjustments compound over time. They reduce vulnerability without adding stress.

- Reviewing savings allocations

- Understanding real returns

- Maintaining flexibility in planning

Final Thoughts

Inflation is not a sudden enemy, it is a constant condition of modern economies. The mistake is ignoring it or reacting emotionally instead of strategically. Awareness changes how you save, spend, and invest.

Once you understand how inflation quietly shapes your money, you gain control over decisions that once felt confusing. Inflation does not require fear, it requires attention, patience, and thoughtful adjustment over time.